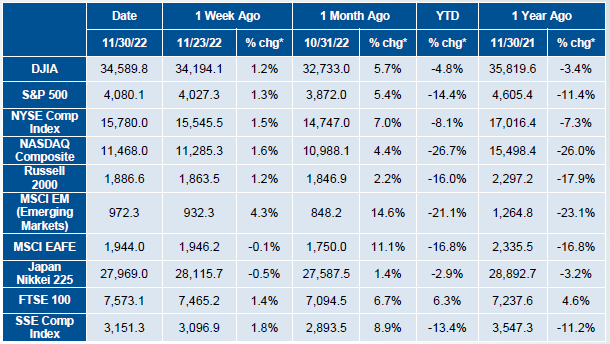

U.S. markets closed higher again in November with the S&P 500 +5.4%, the Dow +5.7%, and NASDAQ +4.4%. There is a continued hope for lower if not a cease of rate hikes by the U.S. Federal Reserve (Fed) in the near term as U.S. inflation numbers improve, giving both stocks and bonds a boost this month.

The U.S. Federal Reserve (Fed) delivered another round of policy rate hikes in November and raised rates by an expected 75 basis points (bps) to 4.0%. October CPI and PPI both came in softer than consensus, while services (especially shelter) remained an area of concern. Investor sentiment improved significantly after the release of these inflation numbers, despite tighter monetary policy.

On the retail sales side, things were better than expected, with sales growth of +1.3% versus previous month. Black Friday, a day of increased retail consumption, returned with its usual sales. Consumers were still spending, though stores needed to incentivize specific merchandise. Third quarter reported a blended earnings growth rate of 2.4% (still lower than the 2.8% expected), highlighting the deteriorating economic backdrop and inflationary pressures, but improved consumer spending signals.

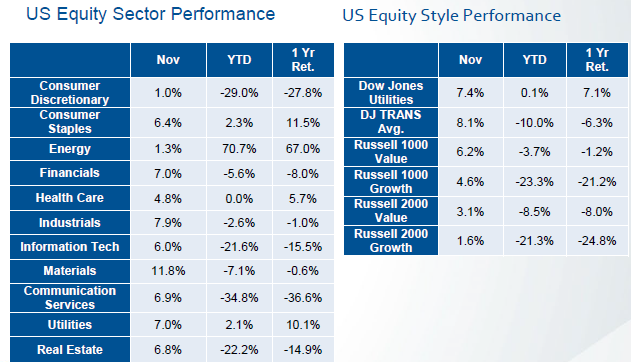

In the remaining month of 2022, the Fed’s monetary policies and its impact, global inflation, and the energy crisis remain in focus. All of the U.S. equity sectors closed higher this month led by gains in Materials +11.8%, Industrials +7.9%, Financials +7.0%, and Utilities +7.0%.

Both Developed International Equities (MSCI EAFE) +11.1% and Emerging Market (MSCI EM) closed higher +14.6%. In China, a fresh surge in new Covid cases reversed initial measures to relax Covid restrictions at the beginning of the month. New restrictions also sparked a series of nationwide protests. Investors remained cautious of China growth given the commitment to zero Covid policies. In the U.K., the Bank of England (BoE) raised rates by 75 bps to 3.0%. The October Eurozone CPI rose 10.6% YoY, a new high, driven mainly by food prices and energy costs. Europe continued to feel the effects of the energy crisis.

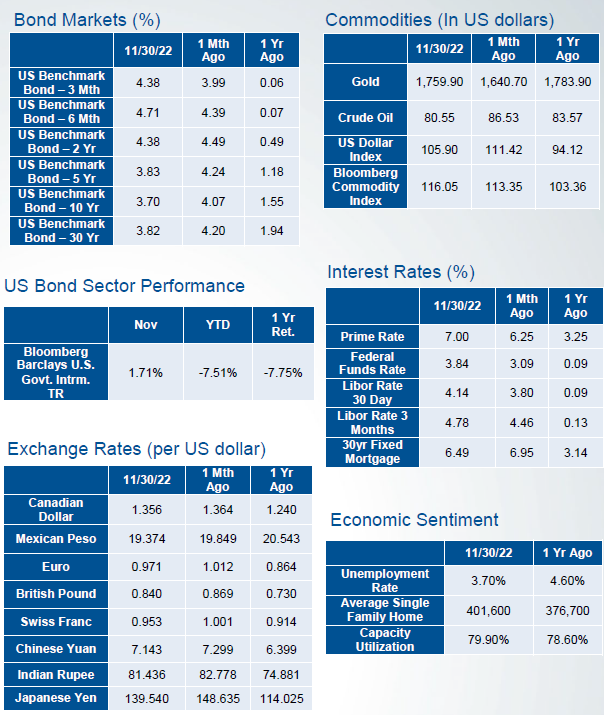

The U.S. yield curve remain significantly inverted even as rates declined this month with the 30Y yield climbing above 4.30% early in the month before dipping below 3.70% at one point in the last week of the month, closing at 3.82%. The U.S. 2-Yr note rose to 4.38% while the 10-Yr fell to 3.70%.

The Bloomberg Commodity Index rose +2.4%. WTI crude oil reversed gains and declined -6.9% at $80/barrel amid worries about China demand and OPEC+ headlines. Brent fell to $85/barrel. Gold reversed losses and had its strongest month since May 2021, up +7.3%.

*Performance for world indices represents price returns (excluding dividends) for the DJIA, S&P 500, NASDAQ, Russell 2000, MSCI EM, MSCI EAFE, NYSE, SSE, and Nikkei, due to data availability.

Not Insured by FDIC or Any Other Government Agency / Not Rockland Trust Guaranteed / Not Rockland Trust Deposits or Obligations / May Lose Value

Investments in stocks, bonds, mutual funds, and other securities are not bank deposits or obligations, are not guaranteed by any bank, and are not insured or guaranteed by the FDIC (Federal Deposit Insurance Corp.), the Federal Reserve Board, or any other government agency. Investments in stocks, bonds, and mutual funds involve risks, including possible loss of principal.