Happy New Year!

From everyone here at IMG we hope you enjoyed your Holiday season and your New Year is off to a great start. 2021 may not have put all aspects of the pandemic in the rear view mirror, especially recently with the emergence of the new Omicron variant. However, investors looked through the uncertainty around Covid and the markets ended the year on a positive note. The S&P 500 achieved its third straight year of growth and corporate profits were supported by strong consumer spending. As we enter 2022, we do so with an underlying positive narrative. Inflation, at least in the short term, will continue to be a headwind the market will need to tame in 2022, but the Federal Reserve (the Fed) is moving toward the first rate hike to offset this challenge.

Before we look ahead, let’s take a moment to look back and review market and economic activities throughout 2021 from our team of experts. For additional in-depth analysis, you may view recordings of our team as they share insights on various local and national media outlets, as well as our weekly The Markets and the Economy email series at www.RocklandTrust.com/Wealth&Investments.

While the pandemic recovery has been a bit lumpier than initially anticipated, 2021 actually turned out to be a better-than-expected year on a number of fronts including: robust equity market returns, the best GDP growth in 37 years, a significant increase in COVID-19 immunity rates, and an improvement in the labor market.

The S&P 500 finished up 28.7% for the year marking the third straight year of double-digit gains. This was largely driven by better-than-expected and record-high year-over-year estimated earnings per share growth of 45.1% (according to Factset estimates). In 2021, companies were lapping weak 2020 comparisons, consumer demand continued to rebound, and companies found innovative ways to reduce costs in this new virtual environment.

We saw significant improvement in the labor market over the course of 2021. The unemployment rate fell from 6.7% at the beginning of the year to 3.9% in the most recent reading. In addition, wage growth has been rising at annualized rates not seen since the 1980s. While that can put greater pressure on corporate profits, it can also increase household discretionary income levels.

| Asset Class | Benchmark | Q4 | 2021 |

|---|---|---|---|

|

US Stocks |

S&P 500 |

11.03% |

28.71% |

|

US Gov’t Bonds |

BbgBarc US Govt Intermediate |

(0.58%) |

(1.69%) |

|

Cash |

BbgBarc US Treasury Bill 1-3 Mon |

0.01% |

0.04% |

2021 was the 10th best calendar year for US equities in the past 50 years. The S&P 500 closed 70 days at record highs, just shy of the 1995 record of 77 days. The S&P 500’s 28.7% return in 2021 was on top of an 18.4% return in 2020 and 31.5% return in 2019, resulting in a three year compound annual return of 26.1% per year! This is the best three year return we have seen since 1999 and the 8th best three year return we have seen dating back to 1926. In addition, 2021 was a year of short and shallow sell-offs and low volatility. The index amazingly experienced no pullbacks greater than 5% throughout the year as investors shrugged off risks such as the Delta variant, supply chain disruptions, and inflation concerns.

From a sector standpoint, cyclical and rate-sensitive sectors such as Energy (+54.6%), Real Estate (+46.2%), and Financials (+35.0%) led markets higher. The Industrials (+21.1%), Staples (18.6%), and Utilities (+17.7%) sectors all had double-digit returns.

From a market capitalization standpoint, Large and Mid-Cap stocks (Russell 1000 +26.5%) significantly outperformed Small Cap Stocks (Russell 2000 +14.82%) in 2021. From a style perspective, Large Cap Growth stocks (Russell 1000 Growth +27.6%), or stocks that are expected to grow sales/earnings faster than the market but tend to trade at higher valuation multiples, slightly outperformed Value stocks (Russell 1000 Value +25.2%) stocks in 2021. However, Small-Cap Value stocks (Russell 2000 Value +28.3%) significantly outperformed Small-Cap Growth stocks (Russell 2000 Growth +2.83%). Value stocks generally tend to outperform Growth stocks in periods of above-trend economic activity and rising interest rates. Value stocks recovered in the first half of 2021 outperforming Growth stocks, however declining interest rates and fears of the Delta variant caused investors to pile back into Growth stocks in the back half of the year.

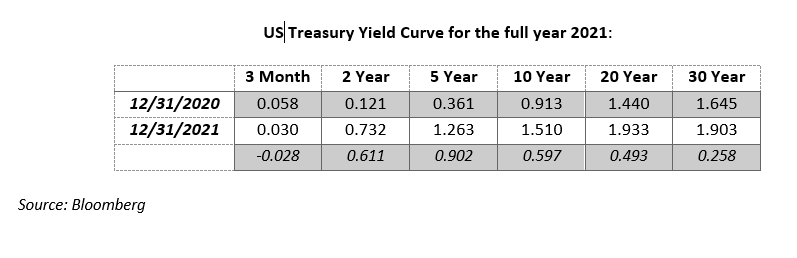

In a year in which the Federal Reserve was left putting out fire after fire, we saw flattening in the yield curve as rates increased particularly in the intermediate range where bonds are more sensitive to the outlook of interest rates set by the Fed. During the quarter, we witnessed a sharp pivot in the Fed’s stance as it took a more hawkish tone at its December meeting and sped up the timeline to end quantitative easing and is now prepared to raise rates several times next year to combat record inflation.

Across the fixed income spectrum returns were mixed for the year. As bond yields moved inversely to prices, we saw negative returns for those asset classes which have stronger links to interest rates and positive returns for those more correlated to credit and inflation. The strongest fixed income performers for the year were high yield debt and Treasury inflation protected securities (TIPS), with both asset classes returning over 5% for the year.

Although strong on an absolute basis, on a relative basis equity diversification was challenged both in the 4th quarter and full year 2021. There were only a handful of diversifying equity asset classes that outperformed the S&P 500 this year- Mid Cap Stocks, Real Estate, and MLPs.

Fixed income diversification, however, was strong in the 4th quarter and for the full year 2021. Nearly every diversifying bond asset class outside of International and Emerging Market bonds outperformed this year.

| Asset Class | Benchmark | Q4 | 2020 |

|---|---|---|---|

|

Foreign Stocks |

MSCI EAFE |

2.69% |

11.26% |

|

Emerging Markets Stocks |

MSCI Emerging Markets |

(1.31%) |

(2.54%) |

|

US Mid Cap Stocks |

Russell Mid-Cap |

6.44% |

22.58% |

|

US Small Cap Stocks |

Russell 2000 |

2.14% |

14.82% |

|

REITs |

MSCI US REIT |

16.32% |

43.06% |

|

Commodities |

Bloomberg Commodity |

(1.56%) |

27.11% |

|

MLPs |

Alerian MLP |

0.55% |

40.17% |

|

Managed Futures |

Credit Suisse Mgd Futures Liquid TR |

1.85% |

8.21% |

|

Foreign Bonds |

FTSE WGBI Non-USD |

(1.98%) |

(9.68%) |

|

Emerging Market Bonds |

JPM EMBI Global |

0.02% |

(1.51%) |

|

US Inflation Protected Bonds |

BbgBarc US Treasury TIPS |

2.36% |

5.96% |

|

Floating Rate Loans |

Credit Suisse Leveraged Loan |

0.71% |

5.40% |

|

US High Yield Bonds |

BbgBarc US Corp High Yield |

0.71% |

5.28% |

|

Convertible Bonds |

ICE BofAML Convertible Bonds |

(0.03%) |

6.34% |

While forecasts for the end of the pandemic have been clouded by variants that appeared this year, there is hope it evolves into an endemic disease. We reflect on 2021 with appreciation for another year of strong stock market returns. As we look forward to 2022, we are hopeful it will become the year we can live with Covid versus living in fear of it. Inflation remains a wild card, but any impact to the stock market and economy will continue to be monitored and reported to you as always with an eye on protecting your financial future. In the meantime, stay safe. Our team is always available to answer any questions and we remain committed to ensuring your investments are appropriately positioned and well-diversified so you can meet your financial goals.

David B. Smith, CFA

Chief Investment Officer

Investment Management Group