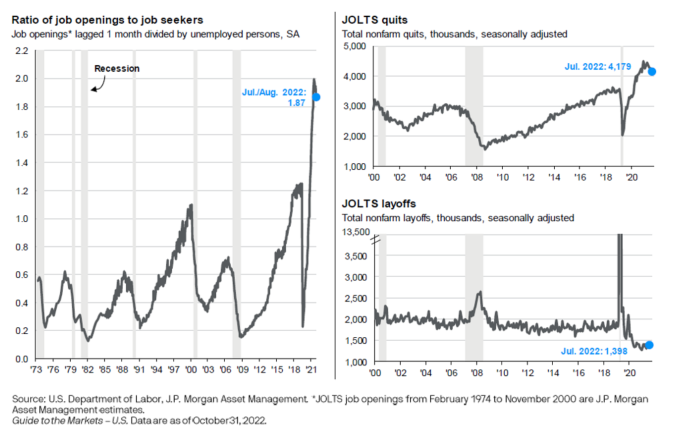

The current unemployment rate is 3.7%, basically hovering near 50 year lows. Employment is arguably the most important barometer for continued consumer spending and therefore growth in the economy, as measured by Gross Domestic Product (GDP). There has become a mounting gap between demand for job openings from employers and supply of workers, as evidenced by the ratio of job openings to job seekers. See the below chart of job openings ratio to job seekers (JOLTS).

Nonetheless the pandemic drove interesting new behaviors in the labor market, particularly on the supply side. For one, many people left the work force, especially those older and nearer retirement. It also forced many dual income families to make more difficult decisions relative to child care and balance of life. In addition, while a large and complicated issue, immigration patterns have become increasingly more volatile, impacting a whole category of jobs that historically have been difficult to fill. Furthermore, individuals have participated in the “Great Resignation” by voluntarily resigning from their jobs, and in “Quiet Quitting”, doing the bare minimum while at work. The result of these behaviors has been fewer workers and reduced productivity.

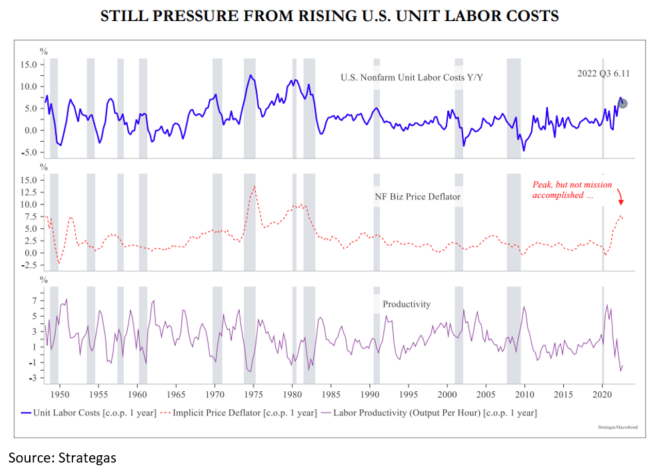

The ongoing gap in employees required versus the pool of potential workers may certainly change. Job openings may decline rapidly in a more challenged, slowing economy. Also, the labor participation rate may increase as individuals potentially reenter the work force. These changes could provide relief to the imbalance in the job market, and possibly slowdown the rate of wage increases. This ultimately is what the Fed hopes to accomplish through its current policy of increasing the Federal Funds rate. The charts below highlight that businesses are still feeling pressure from labor costs. While many may argue wage increases are peaking, it is difficult to know if this is a result of many years of below trend increases, or if this above average level of wage growth will remain.

Reducing upward pressure on wages may be critical to reigning in inflation. This may take some time to happen, so the Fed will continue to raise the Fed Funds rate until it feels confident that inflation is under control. Consequently, we continue to monitor the labor market and its potential impact on future economic growth and corporate profits.

While we remain apprised of the current economic environment, we stay focused on the long term by building well-diversified portfolios able to withstand market downturns.