Written by Steve Andrews

Inflation Continues

The process of disinflation (inflation rising more slowly – not falling) continued in March. Core PCE (Personal Consumption Expenditures - the Fed’s preferred inflation metric) has fallen in six of the last eight months, to 4.6% from year-ago levels, and expectations for future inflation over the next 5 to 10 years remain just above the Fed’s 2% target.Price Index Updates

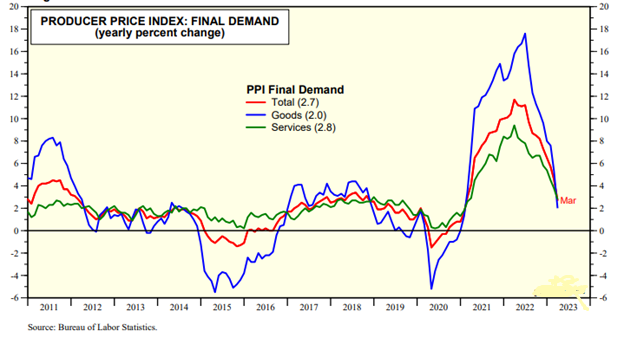

Growth in March Consumer Prices (CPI) eased a full point, from 6.0% to 5.0% while the subset that the Fed has begun to watch closely (“Super Core CPI,” which excludes food, energy, goods, and rents), eased to 7.2% from a year ago – down from 7.6% in February. Meanwhile, Producer Prices (PPI) fell 0.5% in March. As a result, the year-over-year increase in PPI (inflation in the pipeline) slipped to 2.7% from a peak of 11.7% a year ago.

The PPI data supports our belief that rents are the primary cause of inflation “stickiness,” and overall inflation will continue to normalize (head toward the Fed’s 2.0% target) over the course of this year and into next, as rent increases continue to moderate. US housing prices peaked nearly 12 months ago and rents track home prices closely (with a 12 to 18-month lag), so expect inflation data to continue its trend lower and take some pressure off the Fed to “overtighten” US monetary policy.

Feelings from The Fed

The recently released minutes from the Fed’s March 22 FOMC meeting where the Fed lifted short-term rates by a quarter-point (0.25%) showed that FOMC members scaled back expectations for peak rates as they try to balance calming the financial sector jitters from Silicon Valley Bank, et al, with reining-in inflation. Of note, "members anticipated that some additional policy firming may be appropriate.” This was a change in sentiment from the February 1 meeting where "all participants continued to anticipate that ongoing increases in the target range for the federal funds rate would be appropriate". With their assessment of the potential economic effects of the recent developments in the banking sector, FOMC members said that the US banking system is sound and resilient, but that recent developments were likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation, but the extent of these effects was uncertain. Fed staff members projected a mild recession starting later this year, with recovery occurring over the subsequent two years.

We’ve been scratching our heads at the many experts (some at the Fed) who believe that we “need” a recession to stifle inflation. On the contrary, economic growth and productivity are the keys to driving costs lower - just remember the stagflation of the 1970’s. Recessions are all about removing bloat from the economy, like the stock market bubble in 2000, and the housing bubble in 2008, but it’s hard to see much bloat to trim right now.

Housing Rates

Prices aside, it’s not housing. After plummeting to a 50-year low (63%) in the years following the housing crash, the US homeownership rate clawed back to a post-crash high of nearly 68% just before COVID dealt another blow to growth. Despite the recent concern over the housing market from higher mortgage rates and a lack of supply keeping prices elevated, new and existing home sales have been rising over the past few months. This has helped the homeownership rate rebound to 65.9% in Q1, lifting it back above its 65.2% average over the past 50 years.

Consumer Spending

US consumers will likely determine the time and scope of the next recession. They have remained resilient in their spending in the face of all the concerns that have beset them over the past year, but the retail sales (and recent credit card transaction) data are suggesting that some moderation in spending has occurred. We will have to watch to see if this is just a “soft patch” that happens from time to time, or the start of a real spending slump. The employment picture remains bright, with those feeling comfortable enough to quit and find another job at high levels, and households are still sitting on savings that top $1 trillion to backstop rising wages and salaries.

In Conclusion

When (and if) a recession arrives, it will be the most anticipated recession in history. We suspect that a lot of the focus on it is simply to get it over with, like knowing you have to get a tooth filling replaced. Either way, we expect one more quarter-point (0.25%) rate hike in May as the Fed seeks to regain its credibility on fighting inflation but, after that, moderating inflation will put an end to the rate-hiking cycle. The good news is that, over the past 40 years, from the time of their final rate hike, until the Fed transitions (pivots) to the first rate cut in the easing cycle that inevitably follows, the stock market saw (on average) an 11% return, while bonds returned around 7%. In the meantime, let’s celebrate disinflation.