With interest rates suddenly inching up, businesses big and small are considering converting adjustable rate loans to fixed rates. Traditional refinancing methods are always available, but there is another option.

Sophisticated fiduciaries at Fortune 500 companies have for years utilized derivatives known as interest rate swaps in order to better manage monetary risk.

Interest rate swaps are, in their simplest form, an exchange of payments. One party in the swap trades the flexible rate on its debt to a fixed set of interest payments for a number of years - say five percent over 10 years. The other party receives adjustable rate payments, which are indexed to interest rates, usually the one or three month LIBOR rate.

But in practice, interest rate swaps can be complicated and smaller to mid-sized companies might believe the derivatives game is beyond their scope of financial wherewithal or perhaps too risky to manage effectively.

Not so. Today, more banks - and not just the money center banks - offer interest rate swaps to their customers and will take care of all the paperwork, regulation compliance, accounting, and monitoring to make the process as streamlined as possible.

“These are tools being used by the major corporations to reduce risk,” said Michael Bontrager, founder and CEO of Chatham Financial, a global financial advisory services and technology firm based in Kennett Square, Pennsylvania. “Now, banks like Rockland Trust are saying that if you’re a smaller company you can have the same financial options - and protections - as the major corporations.”

In a way, Bontrager notes, banks that are offering rate swaps are “democratizing the ability of more companies to avail themselves of these products.”

Defining Swaps

So what exactly are rate swaps? Why would someone want to use the product? And how do they work?

It starts with the natural inclination of borrowers to generally want fixed-rate loans to better manage their costs and expectations. Banks, however, fund their loans with deposits that have fluctuating interest rates so managing net interest margins can be problematic, especially when short term rates are expected to increase. Therefore, the adjustable rate loans are lower risk and can be more preferable.

This common tension creates markets and opportunities for both banks and borrowers.

“With interest rate swaps we can offer our customers long-term fixed rates but the bank actually retains an adjustable rate,” said Jonathan Nelson, senior vice president and treasurer of Rockland Trust. “It’s a win-win all around.”

It’s a win for borrowers because they can convert some or all of their floating rate debt to fixed rates - good to do in the current rising rate environment - without going through the time and expense of a total refinancing. It’s a win for the bank because it finds a third party wishing to receive the fixed rate, while the bank retains the original adjustable rate. Because swapped loans are lower risk to the banks, the banks can then be more competitive on pricing, passing some of the benefit back to the borrower.

In other words, the borrower is able to hedge their risk by locking in a more competitive long term fixed rate, while the bank takes on an adjustable rate loan that enables them to more adequately manage their margins. Interest rate swaps are traded over the counter, and if a company decides to exchange interest rates, it will need to agree, in theory, with another party on such things as length and terms of the swap. But mostly the bank handles those arrangements and the original borrower is not involved directly in those issues.

Getting Under The Hood

The mechanics of how it’s all done involves several parties - the bank’s customer, the bank, and a counter-party or swap dealer that the bank’s borrower never sees. A large money center bank - such as Deutsche Bank, J.P. Morgan, Wells Fargo or Bank of America - serves as a swap dealer. These are companies that make markets in swap trading and take positions in the swap markets for their own accounts.

Riding herd on all of this are companies like Chatham Financial, which is an independent advisor for both the bank and the customer.

“The advisor is there to make sure pricing is appropriate and the terms are structured properly,” said Rockland’s Nelson. “Some customers may be new to swaps or may feel they don’t have the expertise, so firms like Chatham will guide them through the process.”

Chatham’s Bontrager notes that one of the advantages of a swap is it separates the debt decisions of corporate treasurers from the interest rate decisions.

“Normally, those decisions are made simultaneously,” he said. “Swaps put a lot more control and flexibility in the hands of the treasurer.”

There are other advantages, as well. Fixed rate loans typically carry pre-payment penalties while swaps may carry penalties in a falling rate environment, but they can create a realized gain if rates go up and the borrower elects to terminate the swap.

Greg Vickowski, the chief financial officer of The Procaccianti Group, a privately held real estate investment and management company based in Cranston, R.I, has been utilizing swaps for nearly 30 years. His company buys hotels that are usually under-performing and renovates and re-brands them. Initially, he said, banks are less willing to commit to fixed-rate loans until the property stabilizes.

“At that time we might swap all or some of the debt for a fixed-rate,” Vickowski said. “It’s highly advantageous and certainly less expensive and more efficient than refinancing an entire loan.”

Vickowiski notes, however, that nearly three-fourths of Procaccianti’s debt is in so-called CMBS instruments (commercial mortgage-backed securities) that have little flexibility and are not offered by most traditional banks because they tend to be more complex and volatile than residential mortgage-backed securities.

“There’s a large population that doesn’t want to deal with CMBS shops because it can be slow, impersonal, cumbersome, inflexible and expensive,” he said. “That’s why banks like Rockland can prosper in this market. You can work directly with a banker and develop a relationship and the customer doesn’t have to bother or even know about what’s going on behind the scenes. If banks had the ability to offer CMBS debt, I’d only deal with banks.”

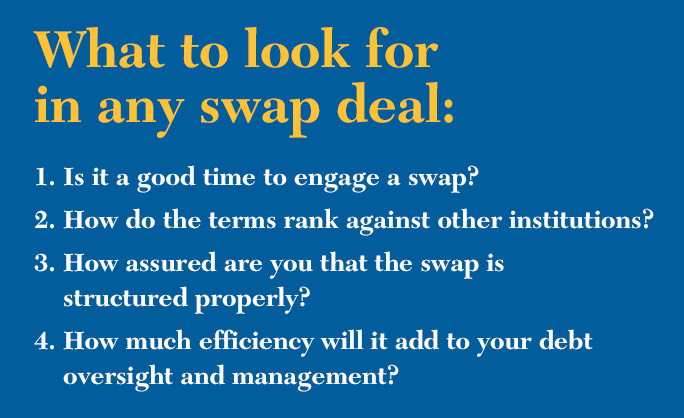

Deciding If Swaps Are The Right Choice

Financial experts say some of the factors in the decision matrix about swaps would include:

- How sensitive is my business to interest rate changes?

- What percentage of my debt is fixed versus fluctuating?

- How much certainty do I have in my borrowing?

- Are there things coming in the next year that could drive up my debt?

“Adjustable rates have done really well over the last 10 years,” said Nelson. “But, given the current direction of short term rates, borrowers may now want to manage some risk by floating only a portion of it and moving some to a fixed rate.”

There are, of course, inherent risks in rate swaps. Chief among them is the fact that interest rates are unpredictable. Swaps carry a market value that fluctuates with market rates. As rates change the borrower may float into an unrealized gain or loss position. If the borrower looks to exit their swap, their position will be monetized. Another risk involves the additional level of complication in managing one’s debt portfolio.

Most of the risks can largely be mitigated by dealing with reputable institutions in strong financial positions and relying on well-established companies to represent the customers and the banks. Rockland Trust has successfully executed more than $1 billion in swap loans since 2009.

With rates on the rise, many experts believe there will be an increased interest in rate swaps.