Dan Landers tells the story often about a small local company looking for financing early in his banking career.

The company had little more than an idea about making orange sneakers for women who were caught up in the burgeoning aerobics craze. Landers’ boss wasn’t impressed, but the company ultimately landed financing by pledging what little inventory it had plus some accounts receivable. And the company, Reebok International, was literally off and running.

“There was a stigma in those days about pledging assets for funding,” said Landers, who now serves as senior vice president and executive in charge of Rockland Trust Asset Based Lending (ABL) group. “Banks and regulators didn’t think it was a safe way to lend and they didn’t really understand it and would be criticized just for offering it.”

Times have definitely changed. Thanks to years of experience as well as new regulations and guidelines, asset-based lending is no longer the purview of lenders of last resort for firms in trouble. Instead, it has become a widely accepted form of credit in the U.S., especially for middle-market companies looking to move forward.

The list of corporations that turned to the financing method reads like a directory of the most successful companies in the country: Hertz, Del-Monte, Neiman Marcus, J Crew and Liz Claiborne. Locally, New Balance, Boston Scientific, Cole Hahn and many others have used ABL as a fundamental financing option. In fact, ABL has broadened in recent years from only providing working capital to acquisition and restructuring financing's.

“Banks should finance companies though all of their cycles,” said Landers. “We need to respond to every kind of company at whatever point in their development and asset-based lending gives us a lot of flexibility beyond the more familiar forms of financing.”

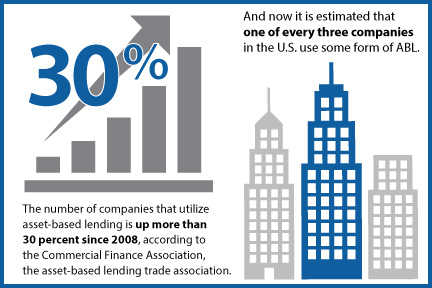

According to the CFA’s ABL Index for the third quarter of 2015, total loan commitments grew seven percent over the same period a year earlier, reflecting stable market conditions.

“I would characterize the quarter as ‘steady,’” said Robert Trojan, chief executive officer of the CFA. “There are minor changes to the various components. Commitments tend to grow the further we get away from the recession.”

For young companies or those going through transitions, the lending door may seem closed if traditional unsecured lines have been exhausted or when raising equity isn’t an option. But asset-based lending may be a desirable choice and, many times, a more economical source of financing. Because the lenders place a heavier reliance upon the assets of the borrower, asset-based lending has the advantage of being a more consistent source of liquidity in volatile markets. Its popularity is also attributable to these features:

- ABL supplies cash to support liquidity needs without the need to wait for receivables.

- ABL is especially desirable for companies that have cyclical or seasonal sales because it can provide liquidity during slow periods and times of inventory buildup.

- Rapidly expanding companies can turn to ABL for cash to fund growth or replenish internal capital.

- ABL is often extended with a limited number of covenants.

- Terms and repayment schedules can be flexible and customized.

60 Million Pounds of Cranberries illustrates Ebbs and Flows

In May 2014, Decas Cranberry Sales Inc., the nation’s second largest cranberry growing, processing and marketing company, secured a $22.66 million asset-based loan from Rockland Trust to refinance a previous loan and for working capital to fuel its growth.

“In our business you have 60 million pounds of cranberries in November and by the following September they’re nearly all gone,” said Decas chief financial officer Norman Beauregard. “So asset-based lending really works well to keep things financially stable though the ups and downs.

Beauregard said the company, which is based in Carver, Mass., worked almost exclusively with national banks during most of its history but came to believe they didn’t fully embrace the volatility of the cranberry agricultural business.

“Having a regional bank gives us a partner in the region who understands the business and the region, he said. “If you hit a blip, they are more likely to understand why.”

Decas’ financing with Rockland consisted of a $2.16 million equipment term loan and a $5.6 million mortgage loans. The bulk of the ABL, some $15 million, provided a working capital line of credit.

“Our plan is to grow and expand, particularly our retail sector,” said Beauregard, “So we needed financing for a minor restructuring.”

A revolving line of credit is the most common type of ABL. Borrowers draw funds, repay draws, and redraw funds throughout the life of the loan. These lines are commonly used to finance short-term working capital assets, usually inventory and accounts receivable. Borrowers with substantial working capital needs, like wholesalers, retailers and distributors, frequently use revolving credit.

Service companies may also depend on revolving credit to fund accounts receivable. The loan is normally secured by working capital assets, though sometimes plant, equipment and even real estate in some situations. The value of the assets determines the loan amounts and the availability of funds.

“Retail companies are prime examples of why asset-based lending works,” said Andrew Wierman, Rockland Trust vice president. “Typically, retailers make most of their money in the fourth quarter so you can’t base credit on cash flow. We can fund companies who have lengthy periods of little or no profit. That’s the beauty of asset-based lending.”

Keys to Success

Experts say the keys to successful asset-based lending are close monitoring and near-constant evaluation, especially during tightened economic conditions when staying appraised on every aspect of the balance sheet is necessary and cash flow is crucial.

“We get daily or weekly reports from our clients,” Landers said. “In some cases we’ll have appraisal firms check the inventory and we send out audit teams quarterly.”

This isn’t as daunting for the borrower as it may sound. Most well-run companies have detailed accounting data and inventory information at hand.

“With non-asset-based you might report once a month,” said Beauregard. “With asset-based lending it is weekly. So it’s a little different than with commercial banking, but we’ve adapted easily and the bank helps along the way.”

As more businesses look for opportunities in a changing economic climate, leveraging and asset-based solution might be a viable way to capitalize.

“Some of our clients probably wouldn’t be in business if it weren’t for asset-based lending,” said Landers. “A lot of solid, stalwart companies started as ABL users and it remains a good, inexpensive form of financing for the young Reeboks of today.”